All Categories

Featured

Table of Contents

Getting rid of representative payment on indexed annuities permits substantially greater detailed and actual cap rates (though still considerably less than the cap rates for IUL plans), and no uncertainty a no-commission IUL plan would press illustrated and actual cap rates greater also. As an apart, it is still possible to have a contract that is extremely abundant in agent settlement have high very early money abandonment values.

I will certainly concede that it is at least in theory POSSIBLE that there is an IUL plan around released 15 or twenty years ago that has actually provided returns that transcend to WL or UL returns (much more on this below), yet it is very important to much better comprehend what a proper comparison would involve.

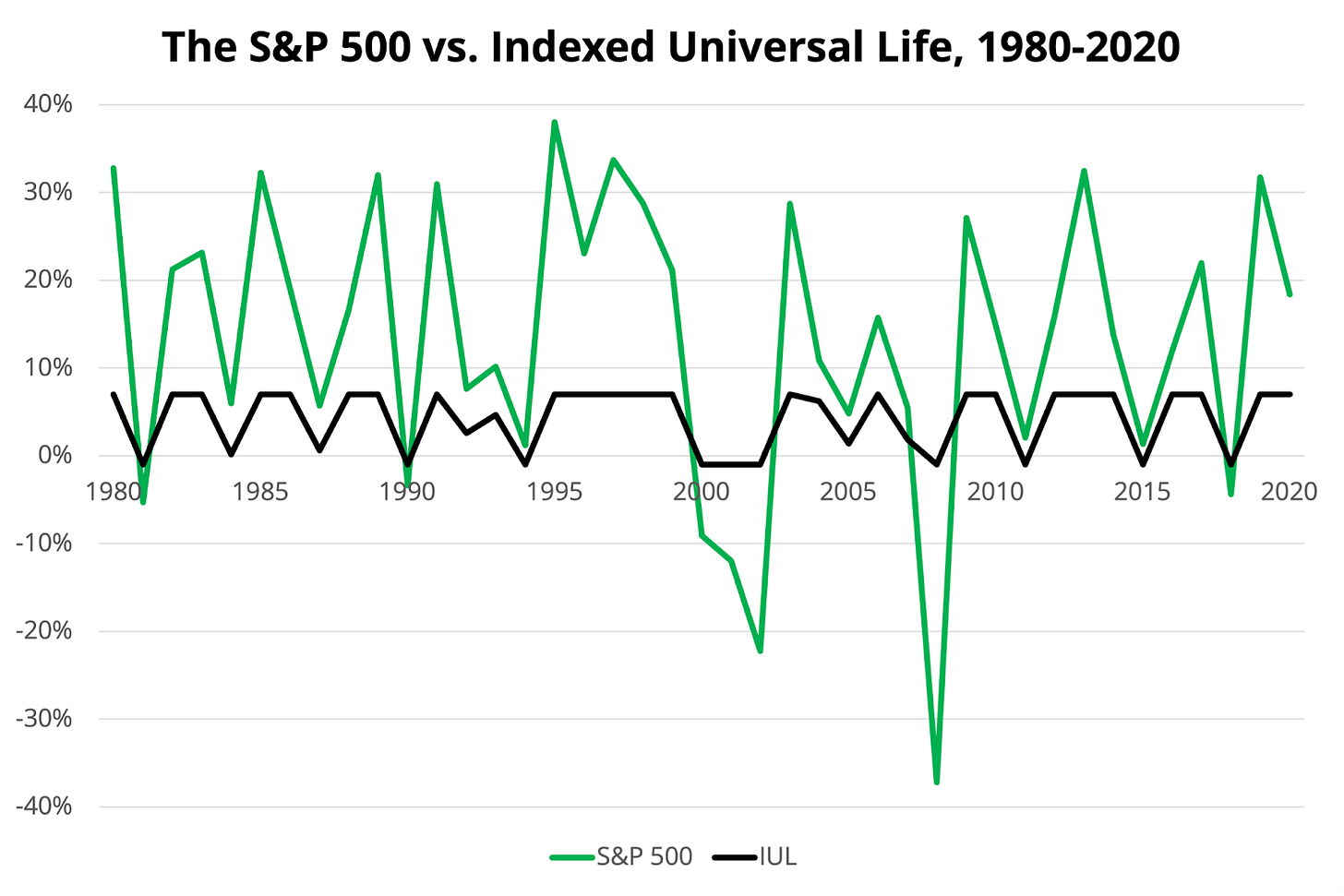

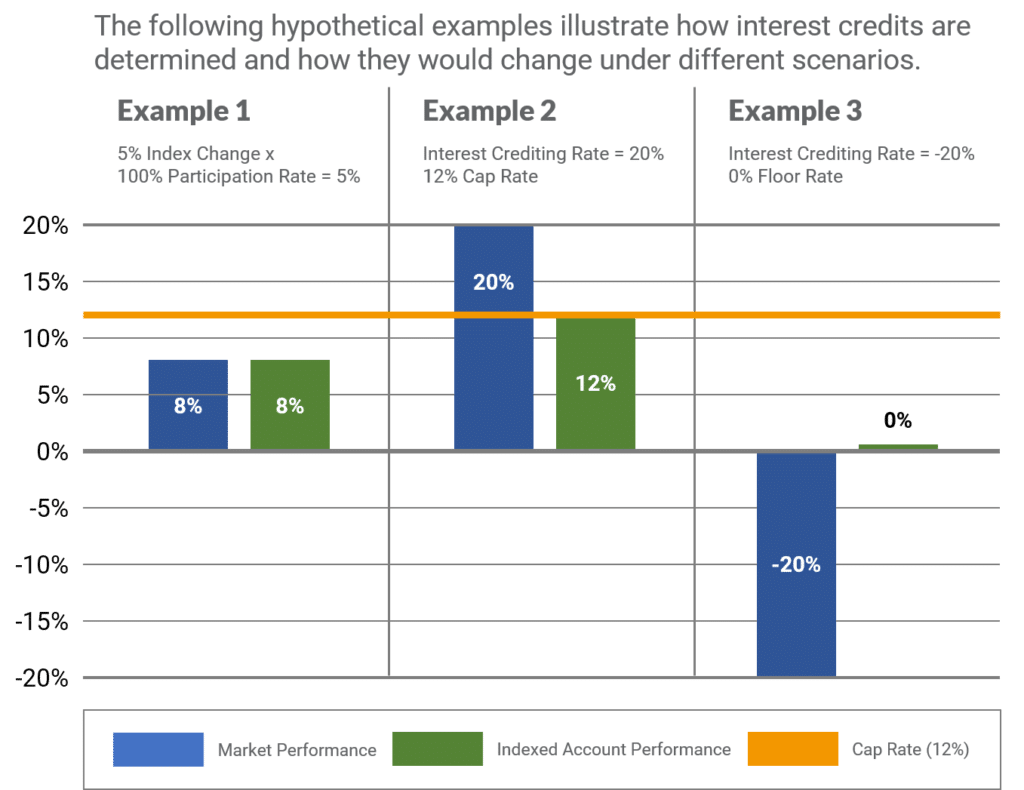

These plans usually have one lever that can be evaluated the company's discretion yearly either there is a cap price that defines the optimum crediting price in that certain year or there is an involvement rate that defines what percentage of any favorable gain in the index will certainly be passed along to the plan because certain year.

And while I typically concur with that characterization based upon the mechanics of the policy, where I differ with IUL advocates is when they identify IUL as having exceptional returns to WL - best variable life insurance. Numerous IUL advocates take it a step further and indicate "historical" information that seems to support their insurance claims

There are IUL policies in presence that lug even more danger, and based on risk/reward concepts, those policies ought to have higher expected and real returns. (Whether they really do is an issue for serious discussion however companies are utilizing this technique to assist justify higher illustrated returns.) Some IUL plans "double down" on the hedging technique and evaluate an extra fee on the plan each year; this charge is after that utilized to raise the alternatives budget plan; and then in a year when there is a positive market return, the returns are intensified.

Indexed Universal Life Insurance Companies

Consider this: It is possible (and actually most likely) for an IUL policy that averages an attributed rate of say 6% over its initial 10 years to still have a total negative rate of return throughout that time due to high fees. Numerous times, I find that representatives or customers that brag concerning the performance of their IUL plans are confusing the credited price of return with a return that correctly reflects all of the policy bills.

Next we have Manny's concern. He says, "My buddy has been pressing me to get index life insurance and to join her business. It looks like a Multi level marketing.

Insurance sales people are okay individuals. I'm not suggesting that you 'd despise yourself if you said that. I said I used to do it, right? That's just how I have some understanding. I made use of to offer insurance at the start of my occupation. When they market a costs, it's not unusual for the insurance provider to pay them 50%, 80%, even often as high as 100% of your first-year costs.

It's difficult to sell since you obtained ta constantly be looking for the following sale and going to discover the following individual. And specifically if you do not really feel extremely founded guilty about things that you're doing. Hey, this is why this is the finest solution for you. It's going to be hard to find a great deal of gratification in that.

Allow's discuss equity index annuities. These points are prominent whenever the marketplaces remain in an unstable duration. But below's the catch on these points. There's, initially, they can control your actions. You'll have surrender durations, normally 7, 10 years, perhaps even past that. If you can not obtain accessibility to your cash, I know they'll inform you you can take a tiny percent.

Which Is Better Term Or Universal Life Insurance

That's just how they know they can take your cash and go fully spent, and it will certainly be fine because you can't obtain back to your cash up until, once you're into seven, ten years in the future. No issue what volatility is going on, they're most likely going to be fine from an efficiency standpoint.

There is no one-size-fits-all when it comes to life insurance policy. Getting your life insurance policy plan best considers a number of variables. [video description: Pleasant music plays as Mark Zagurski speaks to the camera.] In your busy life, economic freedom can seem like a difficult objective. And retired life may not be top of mind, due to the fact that it seems up until now away.

Pension plan, social security, and whatever they would certainly managed to save. But it's not that very easy today. Fewer companies are supplying conventional pension and several business have decreased or ceased their retirement and your capacity to count exclusively on social security remains in inquiry. Also if advantages have not been minimized by the time you retire, social protection alone was never meant to be sufficient to spend for the lifestyle you want and deserve.

Fixed Universal Life

/ wp-end-tag > As part of a sound monetary method, an indexed universal life insurance coverage policy can help

you take on whatever the future brings. Before devoting to indexed global life insurance policy, below are some pros and disadvantages to think about. If you select a great indexed universal life insurance strategy, you may see your cash money value grow in value.

If you can access it beforehand, it might be beneficial to factor it right into your. Considering that indexed global life insurance coverage needs a certain degree of risk, insurance policy business tend to keep 6. This sort of plan likewise uses. It is still assured, and you can adjust the face amount and bikers over time7.

If the picked index does not do well, your cash money worth's development will certainly be influenced. Normally, the insurance policy company has a beneficial interest in executing much better than the index11. Nonetheless, there is typically a guaranteed minimum rates of interest, so your plan's growth will not fall below a certain percentage12. These are all elements to be taken into consideration when selecting the most effective kind of life insurance policy for you.

Since this type of plan is a lot more complicated and has a financial investment element, it can often come with greater costs than various other plans like whole life or term life insurance coverage. If you do not think indexed global life insurance policy is ideal for you, right here are some options to take into consideration: Term life insurance policy is a short-term policy that normally uses coverage for 10 to thirty years.

Iul Life Insurance Reviews

Indexed universal life insurance is a sort of policy that offers extra control and versatility, together with greater cash value development possibility. While we do not use indexed universal life insurance policy, we can give you with more information about whole and term life insurance policy policies. We recommend exploring all your alternatives and talking with an Aflac representative to find the very best fit for you and your household.

The rest is included in the money value of the policy after charges are deducted. The money value is credited on a regular monthly or yearly basis with rate of interest based upon increases in an equity index. While IUL insurance coverage may verify valuable to some, it is very important to comprehend exactly how it functions before acquiring a plan.

{kind=link}

Latest Posts

Universal Underwriting

Index Universal Life Calculator

What Is Indexation In Insurance